Bangladesh Electronic Funds Transfer Network (BEFTN) is the most efficient method of interbank payment system which started its ‘Live Operation’ on 28th February 2011 by Bangladesh Bank. The main objective of BEFTN in Bangladesh is to encourage paperless bank payments in a secure, faster & cost-effective way.

Bangladesh Electronic Funds Transfer Network (BEFTN) is the most effective technique in the development of a modern banking payments system infrastructure in our country. All banks who have BEFTN facilities along with Mobile apps provide this facility to their stakeholders 24/7 to make payments to other bank account holders from home.

Table of Contents

What is BEFTN?

BEFTN is basically a money transfer method from one bank to another directly within a limited time without the physical existence of currency as well as individual. BEFTN till now is the most trustworthy, secure and efficient funds transfer system which accelerates the settlement of inter-bank payments, clearing and electronic credits and debits.

Read Also: Advantages of RTGS in Banking? And its regulations in Bangladesh.

BEFTN facilitates the payments system between the banks electronically, which makes it a faster and efficient means of inter-bank clearing over the existing lengthy paper-based system.

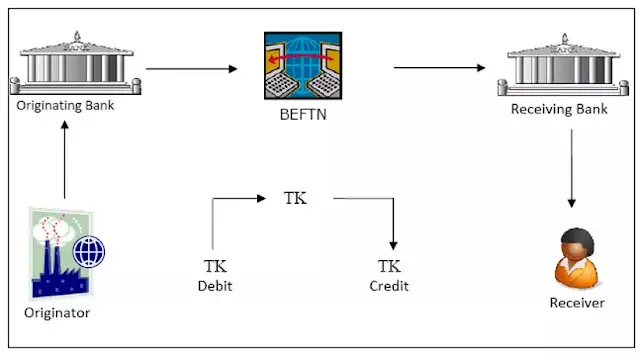

The Participants in BEFTN transaction:

For making a successful BEFTN transaction there involve the following participants:

a) Originator.

Originator is an individual or organization who agrees to initiate EFT entries into the network according to an agreement with a receiver.

b) Originating Bank (OB)

The bank receives instructions whether it is debit or credit from the originator (Must be an account holder of the bank) and forwards the entry to the EFT operator.

c) Bangladesh Electronic Funds Transfer Network (EFT Operator)

Bangladesh Bank act as a clearing authority who receives instructions from originating banks then delivers the instructions to appropriate banks and facilitates the settlement functions.

d) Receiving Bank (RB)

The receiving bank will receive EFT instructions from Bangladesh Bank (EFT Operator) and make necessary arrangements to deposit the instructions to the desired account.

e) Receiver

The receiver is the person/organization who maintained an account with the Receiving Bank whom the instructions for EFT entry were made.

f) Correspondent Bank

A Correspondent Bank’s function is to create EFT files on behalf of the Originator or act on behalf of an Originating Bank or Receiving Bank.

Types of BEFTN Entry:

Usually, there are two types of BEFTN entries practiced in our country. These are;

1. Inward BEFTN

2. Outward BEFTN

Both two types are further divided into two according to transaction mode.

1. Credit Entries

2. Debit Entries

BEFTN Credit Entries

Credit entries take place when the originator (account holder/customer of the originating bank) agrees to transfer funds from his/her bank account into a Receiver’s (account holder/customer of the receiving bank) bank account. Credit entries mostly occur for:

- Inward Foreign remittances

- Domestic remittances

- Payroll private and government

- Dividends/Interest/Refunds of IPO

- Business to business payments (B2B)

- Government tax payments

- Government vendor payments

- Customer‐ initiated transactions

- Sanchayapatra interest transfer.

BEFTN Debit Entries.

EFT debit entries occur when the originator (account holder/customer of the originating bank) wants to collect funds from the Receiver’s (account holder/customer of the originating bank) bank account into his/her bank account. Some examples of EFT debit entries are:

- Utility bill collection

- Equal Monthly Installments (EMI) collection

- Government tax collection

- Government license fees collection

- Insurance premium collection

- Mortgage payments collection

- Club/Association subscriptions

- Payment of loan installment.

BEFTN approved Currencies:

Following currencies are allowed for making a BEFTN transaction.

I. Bangladeshi Taka (BDT)

II. US Dollar (USD)

III. Great Britain Pound (GBP)

IV. EURO (EUR)

V. Canadian Dollar (CAD)

VI. Japanese Yen (JPY)

Steps for originating a BEFTN transaction Instruction:

In case of the Bank, for making a BEFTN transaction originator/customer have to provide the following data and also have to ensure the genuineness of the provided data;

- Have to provide the desired currency mode for making BEFTN transactions.

- Originator account number from which account he agreed to make the BEFTN transaction.

- Transaction mode whether it is debit instruction or credit instruction.

- Originator contact number which is provided at the time of account opening.

- Beneficiary/receiver name.

- Beneficiary Bank account name with his bank and branch name and Detail address of the bank.

- Routing number of the bank in which the beneficiary maintained his account.

- Transaction amount.

But in the case of Mobile apps customers are solely liable for making or initiating a BEFTN transaction. Here, first,

- You have to log in to the app by putting your log in credentials.

- Then have to go to the BEFTN dedicated menu and click on BEFTN.

- Have to select your source account from which account you have made the transaction.

- Then select Beneficiary account box and type Beneficiary Account title, Beneficiary Account Number, Beneficiary Bank name, Branch Name, Routing number of the bank, District, Amount correctly.

- Then press the “Pay Now” or “Process” button.

BEFTN Return Reason

BEFTN transaction will be returned if the following criteria are found;

01. If the receiver Account is Closed.

02. No Account/Unable to Locate Account.

03. In case of Invalid Account Number.

04. If Originating bank requested to return the BEFTN entry.

05. If the Beneficiary or Account Holder Deceased.

06. If the receiver Account is Frozen, Dormant or inoperative.

07. If BEFTN transaction initiated for a Non-Transaction Account.

08. If the receiver of the debit transaction marked his account stop payment.

09. Invalid Company Identification, Invalid Individual ID Number.

10. If the Originator provided a consumer account to make debit BEFTN transaction has not been authorized to debit.

11. If the amount of debit transactions is in the process of collection (i.e., uncollected checks).

12. Duplicate entry.

13. Incorrect Routing Number.

14. If credit Entry Refused by the Receiver, because of;

i. Minimum amount required has not been remitted by the customer;

ii. The required amount by the receiver has not been remitted.

iii. The account is subject to litigation;

iv. BEFTN Amount is too big or results an overpayment;

v. If the originator is not known to the Receiver;

vi. Payments must be returned if the receiver has not authorized this credit entry to this account.

vii. The same day of receipt of the request by the Receiving Bank, made by the Originator/OB;

viii. Within one hour of receipt of the original payment where RB detects it as an erroneous payment.

Transaction limit

Transaction limit for BEFTN are as follows;

- Minimum Tk. 500/- per transfer (But in Mobile app few banks are allowing minimum 10/- for transfer)

- Maximum Tk. 1,00,000 (One Lac) per transfer

- Maximum Tk. 5,00,000 (Five Lac) per day

- Maximum 10 transfers per day

FEES AND CHARGES

No charge is applicable for initiating a BEFTN transaction.

BEFTN Payment Schedule:

| Payments made to other banks before 12.00 PM | Transferred on the same day |

| Payments made to other banks after 12.00 PM | Transferred on the next business day |

| Payments made to other banks during holidays and weekends | Transferred on next business day |

Advantages of BEFTN in Bangladesh

1. Smooth payment system among all the branches across the country.

2. It will ensure a highly secured payment service since there will be no chance of alteration unlike in the case of the existing paper-based system.

3. It will be efficient since it is paperless & automated. It will optimize the bank’s cash flow management process and working capital cycle.

4. Reduce Administrative Cost (Printing)

5. Elimination of Lost and Stole instruments

6. Reduce Clearing Cost

7. Reduce Fraud

8. Increase Efficiency & productivity

9. Save Time

10. Simplifies Reconciliation

11. Eliminate cheque procurement costs

Disadvantages of BEFTN in Bangladesh

- BEFTN is the most critical component in the development of a modern payments system infrastructure.

- When an amount is transferred through BEFTN, the bank cannot reverse the transaction. You have to submit your complaint to the originating bank they may take a few days to resolve the complaint and refund it. But if the receiver is denied to refund it originating bank nothing has to do.

FAQs:

01. What does BEFTN mean?

Full form of BEFTN is Bangladesh Electronic Funds Transfer Network.

02. How long will BEFTN transfer take to settle?

Usually to settle a BEFTN transaction takes 48-72 hours.

03. Can a BEFTN transaction be reversed?

Reversal of a BEFTN transaction is not an easy process. You may contact your mother bank and lodge a complaint to enquire if they can contact the receiver and recall the funds from them you can get your money back.

04. Is BEFTN free?

Its free of charge. You can initiate a BEFTN transaction for free either from a bank or from a Mobile Apps.

What is the Minimum limit for Sending BEFTN?

Minimum Tk.500/- will be allowed for BEFTN transaction.